Introduction and Objective

The goal of this project is to predict future foreign exchange rates using Recurrent Neural Networks (RNNs), a type of deep learning model well-suited for sequence prediction tasks.

Modeling Strategy and Methodology

The RNN architecture is designed to capture temporal dependencies in the data. The model is formulated as:

Here, \( h_t \) is the hidden state at time \( t \), \( x_t \) is the input at time \( t \), \( W \) represents weight matrices, and \( \sigma \) is the activation function.

Data preprocessing includes Min-Max scaling, expressed mathematically as:

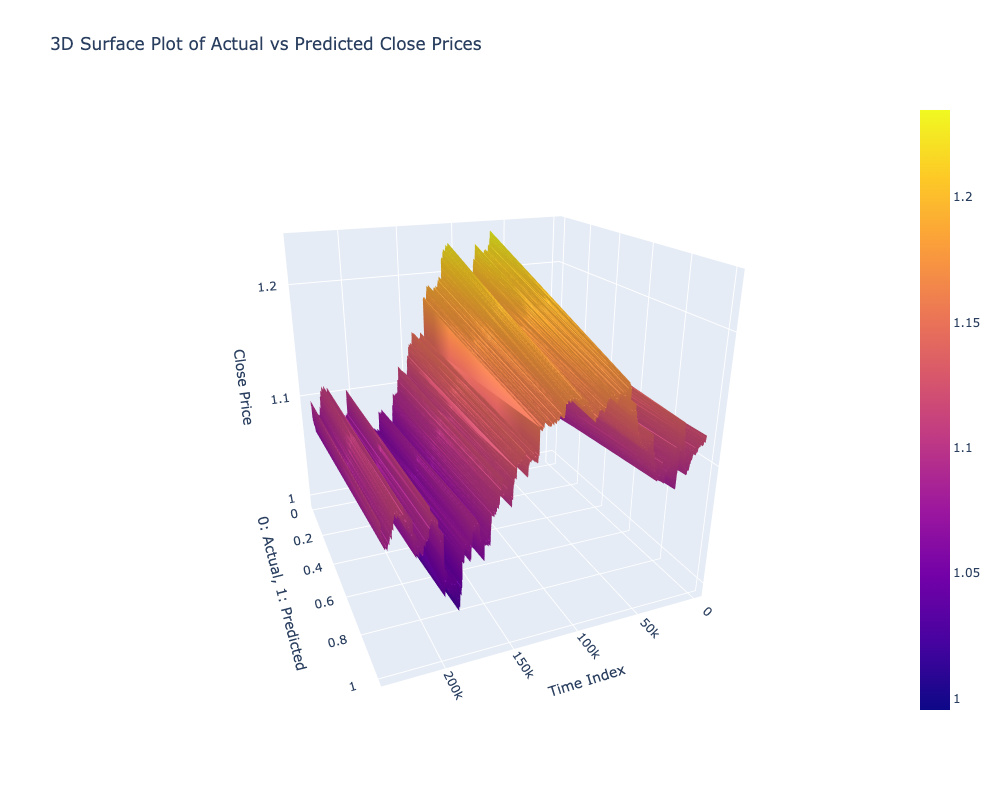

Results and Insights

The model demonstrated robust performance in predicting forex price movements. The predicted and actual prices closely followed each other, validating the model's accuracy. The use of an interactive Plotly graph allowed for an in-depth analysis of model predictions.